Key Takeaways:

- BNPL allows shoppers to purchase instantly and pay later in smaller, manageable instalments, making premium products more accessible without upfront strain.

- India’s BNPL boom is driven by low credit card penetration and the spending habits of millennials and Gen Z.

- D2C brands like Neeman's have seen a 18%+ lift by displaying EMI options upfront.

- For e-commerce brands, BNPL reduces cart abandonment, boosts conversions, and increases AOV without heavy discounting.

- Providers like Snapmint handle credit risk and pay merchants upfront, ensuring zero financial liability for brands.

- BNPL offers a psychological advantage by reducing purchase hesitation, aligning payments with monthly budgets, and delivering instant gratification.

What Is BNPL and How Does It Work?

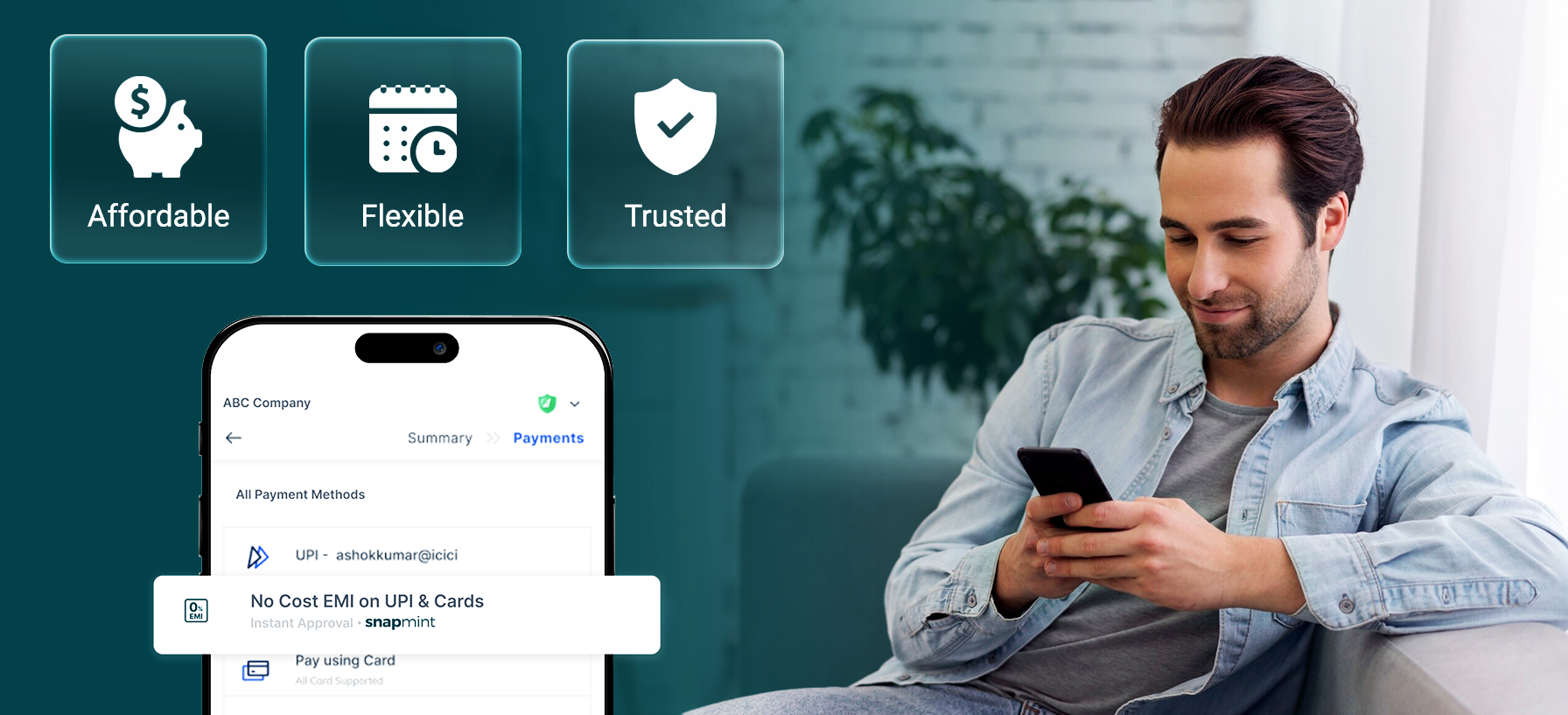

Buy Now, Pay Later (BNPL) is a short-term financing solution that enables consumers to purchase goods and services immediately and pay for them in instalments over a defined period - often at zero or minimal interest.

Unlike traditional credit options, BNPL services often require no credit card, paperwork, or lengthy approval process.

Here’s how BNPL services work for a shopper:

- At checkout, the shopper selects the BNPL option, completes a quick verification (usually via mobile OTP), and receives instant approval.

- The purchase is processed immediately, while the customer repays the amount in monthly instalments, depending on the provider’s offering.

From a merchant’s perspective, BNPL providers like Snapmint disburse the full order amount upfront and take on the credit and default risk, ensuring guaranteed revenue without financial liability.

Why is BNPL on a Boom in India?

India’s BNPL market is witnessing rapid growth driven by a unique blend of rising digital adoption, evolving consumer expectations, and gaps in traditional credit infrastructure.

As you are aware, the youth of India is turning to EMIs as a smarter way to afford aspirational purchases without upfront financial strain.

With low credit card access and high UPI adoption, cardless EMIs offer an easy, accessible alternative. Gen Z and millennials prefer flexible, short-term credit that fits their lifestyle and monthly budgets.

Key Drivers Behind BNPL’s Surge in the Indian Market

Here are some factors that drive the growth of BNPL in the Indian market, especially for D2C, e-commerce, and retail brands:

1. Young Demographic

Millennials and Gen Z, who make up a large share of online shoppers, prefer convenience and flexibility over conventional lending. BNPL aligns with their spending behavior by making high-ticket items feel more affordable.

According to the Home Credit India survey, 60 % of the shoppers, mainly millennials or Gen Z from the tier 1 and tier 2 cities were interested in EMIs for affordable financing, to shop for consumer products, home appliances, and even home renovation.

2. Growth of UPI and Mobile Commerce

India saw a huge jump in UPI transactions. BNPL providers that integrate with UPI offer a familiar, trusted payment flow that boosts adoption among Tier 2–5 consumers.

3. E-commerce Boom and Price Sensitivity

As online retail grows, customers are looking for value without upfront financial strain. BNPL gives brands the ability to sell more, without discounting or margin erosion.

4. Affordability Without Compromise

EMIs allow younger shoppers to access aspirational products, be it electronics, fashion, or beauty categories, without paying the full cost upfront. It breaks high prices into manageable chunks, making premium feel attainable.

Benefits of BNPL for E-commerce & Retail Stores

BNPL isn't just a payment option; it’s a powerful growth lever for e-commerce brands.

By breaking down large purchases into smaller, interest-free instalments, BNPL helps reduce cart abandonment, improve conversion rates, and increase average order value (AOV).

It’s especially effective in a price-sensitive market like India, where offering flexible, cardless credit gives brands access to a wider audience without needing to discount.

Plus, providers like Snapmint take on the credit risk while disbursing full payment upfront, making it a win-win for both shoppers and sellers.

Here’s basically why your D2C brand needs buy now, pay later (BNPL) option:

- Drives Growth: BNPL is more than a payment option; it’s a revenue accelerator.

- Reduces Cart Abandonment: Smaller, interest-free instalments ease purchase anxiety.

- Boosts Conversion & AOV: Shoppers spend more when payments feel affordable.

- Protects Margins: Grow sales without resorting to heavy discounts.

- Expands Reach: Especially effective in India’s price-sensitive, credit-light market.

- Zero Risk for Brands: Snapmint disburses full payment upfront and handles credit risk.

![[Desktop] CTA Button - Unlock 25% Higher Basket Sizes with 0% EMI](https://www.snapmintbusiness.com/hs-fs/hubfs/%5BDesktop%5D%20CTA%20Button%20-%20Unlock%2025%25%20Higher%20Basket%20Sizes%20with%200%25%20EMI.jpg?width=830&height=283&name=%5BDesktop%5D%20CTA%20Button%20-%20Unlock%2025%25%20Higher%20Basket%20Sizes%20with%200%25%20EMI.jpg)

Psychological Advantage: Why Customers Love BNPL

BNPL is not just about affordability; it has a deeper psychological advantage for brands. BNPL targets the psyche of Indian consumers, making them more likely to buy a higher ticket item from your brand. BNPL appeals to the modern shopper’s desire for affordability, flexibility, and instant gratification.

Here’s the science behind the success of BNPL:

1. Affordability That Fits Their Budget

BNPL allows customers to split their payment into smaller, manageable instalments, making it easier to afford high-ticket items without financial strain. Instead of ₹6,000 upfront, a ₹2,000/month plan feels more realistic and attractive.

2. Flexible Payment, Greater Control

Shoppers appreciate the flexibility to choose the number of EMIs and repayment timeline. It gives them control over their spending, aligning purchases with their monthly cash flow, without sacrificing their lifestyle.

3. Instant Gratification Without Guilt

BNPL satisfies the shopper’s desire for instant access to products, especially in fashion, gadgets, or lifestyle categories. They get the product now and pay later, reducing the hesitation that often comes with premium pricing.

4. Reduces Psychological Friction

The high psychological load of paying a lump sum can cause decision paralysis. BNPL eases this tension by lowering the mental ‘cost’ of buying. Customers perceive instalments as less risky and more justifiable.

How to choose a BNPL partner in India?

For forward-thinking e-commerce and D2C brands, enabling BNPL isn’t just a short-term sales tool; it’s a long-term strategy to grow revenue, build loyalty, and tap into India’s next wave of digital shoppers.

Choosing the right Buy Now, Pay Later (BNPL) partner can directly impact your brand’s conversion rate, customer experience, and overall profitability. So, here are a few things you should look for in your BNPL provider:

- High Customer Reach

- Seamless Integration

- Merchant Risk Management

- Regulatory Compliance and Credibility

Why Snapmint is India’s BNPL Growth Partner

In India’s competitive e-commerce landscape, affordability and convenience have become key drivers of purchase decisions. That’s where Snapmint enters the picture.

Snapmint empowers brands to increase Add-to-Cart, Average Order Value (AOV), checkout conversions, and GMV by enabling Buy Now, Pay Later (BNPL) and 0% EMI options that make high-value purchases accessible to a wider audience, without adding any financial risk to the merchant.

0% EMI, wide acceptance in e-commerce

Seamless integration across leading e-commerce platforms and payment gateways.

Proven results for top D2C brands

Brands partnering with Snapmint see up to a 25% - 30% increase in add-to-cart, up to 40% uplift in AOV, and 30% increase in checkout rates.

Handles credit + payouts with zero risk for merchants

Snapmint handles credit checks, risk assessment, and payouts directly. Merchants get upfront settlements, while Snapmint manages customer repayments.

Future of Buy Now Pay Later (BNPL)

BNPL is the future for the Indian market. BNPL is no longer a trend; it’s reshaping how India shops, especially online.

With the e-commerce sector booming, credit card penetration still low, and UPI usage at an all-time high, BNPL is set to become a core payment method across sectors.

Experts predict that BNPL will move from an alternative payment option to a default choice at checkout, especially in fashion, electronics, beauty, and lifestyle.

For forward-thinking e-commerce and D2C brands, enabling BNPL isn’t just a short-term sales tool; it’s a long-term strategy to grow revenue, build loyalty, and tap into India’s next wave of digital shoppers.

This is where Snapmint comes into the picture. Partner with Snapmint, a BNPL company, to unlock long-term growth for your business.

Ready to unlock growth with BNPL?

Book a Free Demo with Snapmint Today.

![[Desktop] CTA Button - Affordability that Unlocks New Revenue](https://www.snapmintbusiness.com/hs-fs/hubfs/%5BDesktop%5D%20CTA%20Button%20-%20Affordability%20that%20Unlocks%20New%20Revenue.jpg?width=830&height=283&name=%5BDesktop%5D%20CTA%20Button%20-%20Affordability%20that%20Unlocks%20New%20Revenue.jpg)